Lloyd's South Africa: Revised policyholder protection rules

The revised Policyholder Protection Rules in South Africa to become effective on 01 January 2018 will have an effect on the managing agents doing coverholder business in South Africa

The South African Registrar for Financial Services, the Financial Services Board (FSB), has tabled the proposed replacement of the Policyholder Protection Rules (PPRs) made under the Long-term and Short-term Insurance Acts in parliament. These replacement PPRs give effect to a number of conduct of business reforms. These reforms should be read together with the amendments to the existing Regulations of the Insurance Acts. The amendments to the Regulations and the PPRs are part of the move to ‘Twin Peaks’ regulation and the implementation of the Treating Customers Fairly (TCF) approach to improve customer protection in the financial services industry.

The conduct of business reforms which will be given effect through the PPRs include Retail Distribution Review (RDR) and proposals of the Ombud for Long-term and Short-term Insurance relating to improved policyholder protection.

Implementation details

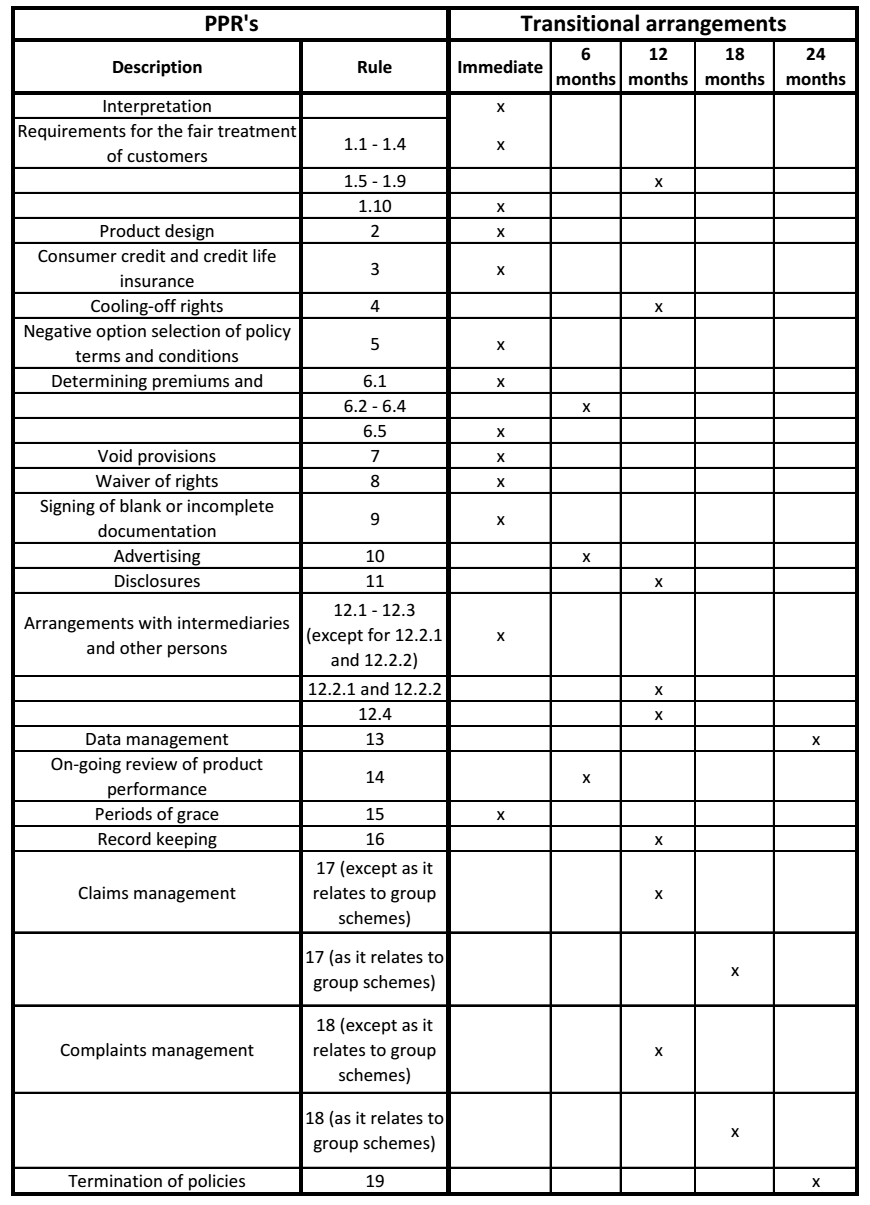

Although certain of the Rules will be effective immediately, the Regulator has allowed a transitional period for the implementation for some of the rules. The attached table provides details of the effective dates for the various Rules.

{kind=link}

Managing agents and coverholders should review the revised PPRs and ensure the potential impact on their business activities are fully understood to allow appropriate action to be taken where required to enable compliance.

Background

Informed by a sector-wide commitment to aligning industry incentives with the principles of fair customer treatment, the purpose of these revised Rules is to guide short- and long-term insurance companies in providing customers with less complex, good-value products to assist them when unforeseen life events happen which often result in economic hardship and poverty. To that end, the PPRs deal with the products, product performance and acceptable service, advertising and disclosure, intermediations and distribution, post-sale barriers and administration.